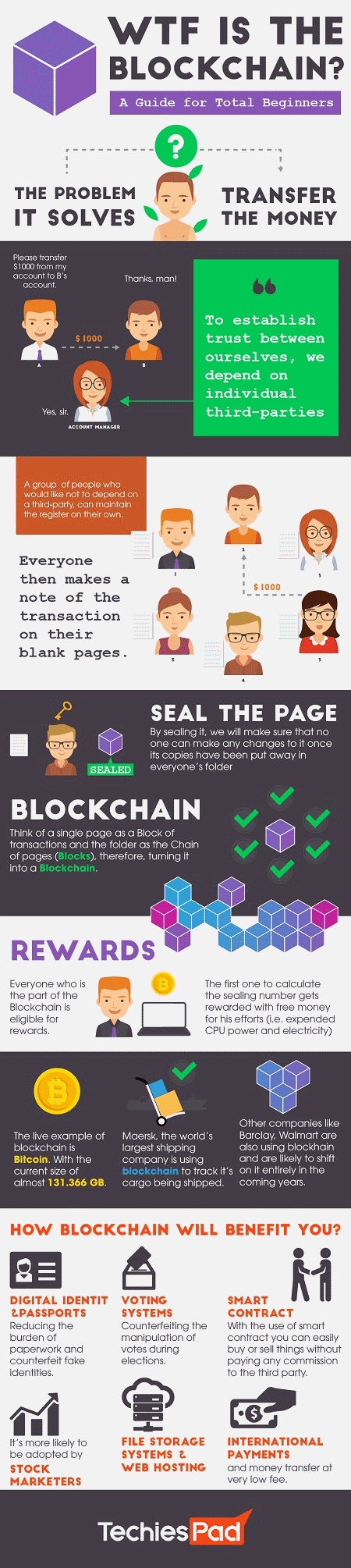

Blockchain technology has emerged as a powerful tool in the fight against fraud and data tampering. Unlike traditional centralized systems, blockchain operates on a decentralized network, making it extremely difficult for malicious actors to manipulate or alter data. This revolutionary technology has the potential to transform industries by ensuring the integrity and security of transactions and information.

By using blockchain, organizations can eliminate the need for intermediaries in transactions, thereby reducing the risk of fraud. Blockchain’s transparent and immutable nature allows for real-time verification of information, providing a high level of trust and accountability. Additionally, the distributed ledger system of blockchain ensures that any changes made to the data are recorded and visible to all participants, making it nearly impossible for fraudsters to tamper with records undetected.

The Role of Blockchain in Preventing Fraud and Data Tampering

Blockchain technology has emerged as a powerful tool in the fight against fraud and data tampering. With its decentralized and transparent nature, blockchain provides a secure and immutable record of transactions, making it an ideal solution for industries that are vulnerable to fraud, such as finance, supply chain management, and healthcare. By leveraging the features of blockchain, organizations can reduce the risks associated with fraud and ensure the integrity and authenticity of their data.

One of the key advantages of blockchain in preventing fraud is its ability to provide a transparent and immutable ledger. In a traditional centralized system, data is stored and controlled by a single entity, making it susceptible to manipulation or tampering. However, in a blockchain network, data is replicated and stored across multiple nodes, making it nearly impossible to alter or forge information without the consensus of the network. This decentralized nature of blockchain ensures that every transaction is recorded and verified, creating a high level of trust and transparency.

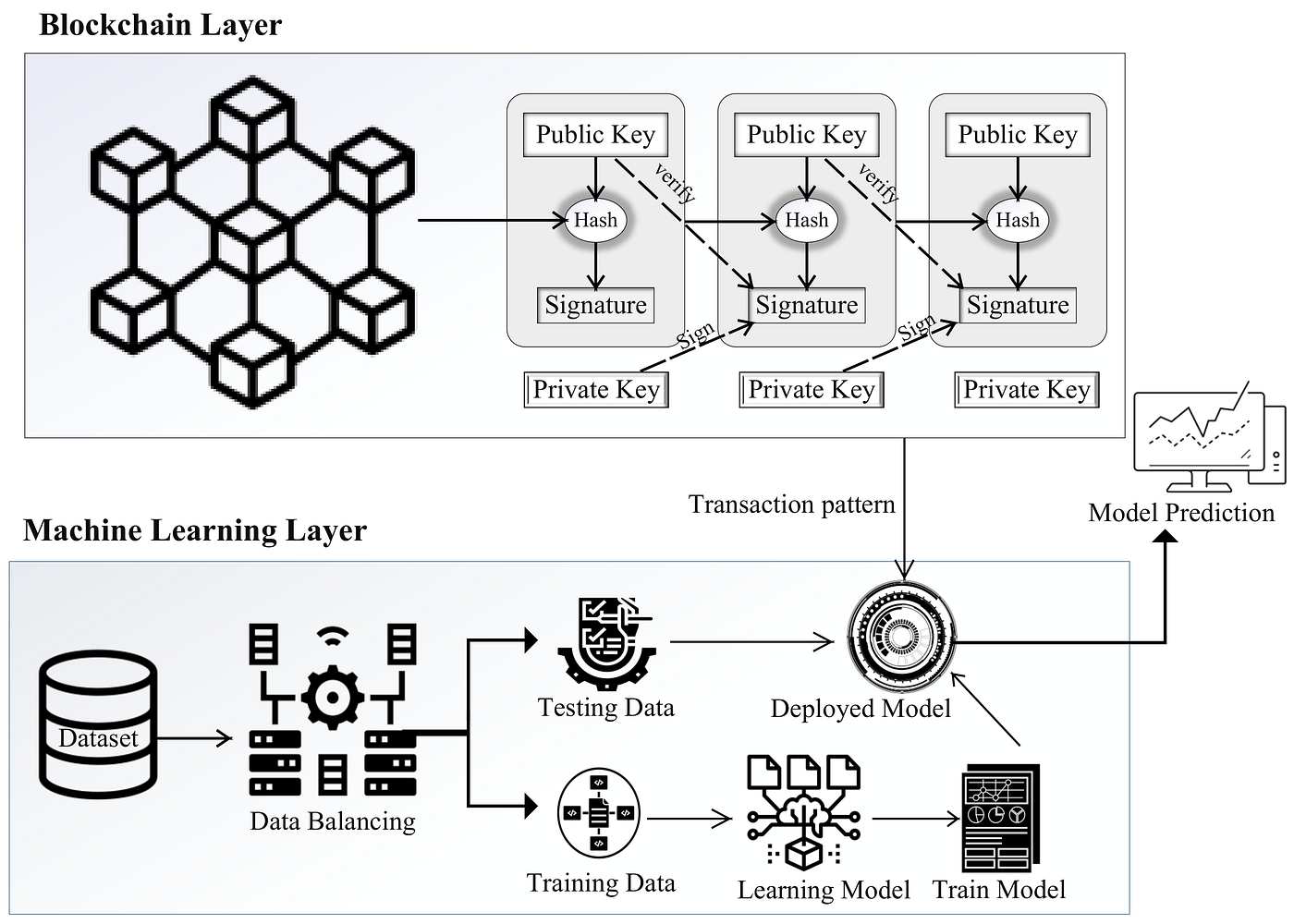

Moreover, blockchain uses cryptographic algorithms to secure transactions and protect sensitive data. Each transaction is encrypted and linked to the previous transaction, forming a chain of blocks that can only be accessed with the correct cryptographic key. This ensures that data stored on the blockchain is secure and resistant to tampering. Any attempts to modify or tamper with a block will be immediately detected by the network. This cryptographic security makes blockchain an ideal solution for preventing fraud and data tampering.

To further enhance the security of blockchain, organizations can implement best practices and development tools. Building a decentralized app (DApp) on a blockchain network requires careful consideration of security measures. Organizations can refer to the article on “Building a Decentralized App: Best Practices and Development Tools” for valuable insights and practical advice on how to ensure the security and integrity of their DApps (Thoughts.tech, 2023). This article provides detailed information on the tools and practices that developers can implement to prevent fraud and data tampering in their blockchain applications.

Blockchain in Finance: Preventing Fraud and Enhancing Security

The financial industry has been significantly impacted by fraud and data tampering. From unauthorized transactions to identity theft, the risks faced by financial organizations are substantial. However, blockchain technology presents an opportunity to mitigate these risks and enhance the security of financial transactions.

1. Securing Transactions with Blockchain

Blockchain provides a secure platform for financial transactions by leveraging its decentralized and immutable nature. By storing transaction records in a distributed ledger, blockchain eliminates the need for intermediaries and reduces the risk of fraud. Every transaction is recorded and verified by multiple nodes, ensuring its authenticity and integrity. This transparent and tamper-resistant system instills trust in financial transactions, benefiting both individuals and businesses.

Additionally, blockchain technology enables the use of smart contracts, which are self-executing contracts that automatically enforce the terms and conditions of an agreement. Smart contracts eliminate the need for intermediaries and ensure that transactions are carried out as intended, without the risk of manipulation or fraud. This automated and secure method of executing transactions reduces the chances of fraud and enhances the efficiency of financial processes.

2. Identity Verification and Fraud Prevention

Identity theft and fraud are major concerns in the financial industry. However, blockchain technology can play a significant role in preventing these fraudulent activities. By using blockchain-based identity verification systems, financial institutions can create a digital identity for individuals that is secure, tamper-proof, and easily verifiable.

Blockchain allows for the decentralization of identity information, eliminating the need for centralized databases that are vulnerable to hacking and data breaches. Individuals have control over their own identity information, and institutions can verify their identity without compromising data security. This enhances the security of financial transactions and reduces the risk of fraud.

Furthermore, the use of blockchain in Know Your Customer (KYC) procedures can streamline identity verification processes and prevent identity theft. KYC procedures require individuals to provide various identification documents and undergo extensive verification processes. By leveraging blockchain, institutions can securely store and share verified identity information, reducing duplication of efforts and enhancing efficiency.

3. Auditing and Transparency

Blockchain’s transparent and immutable nature makes it an ideal solution for auditing and ensuring transparency in financial transactions. Financial organizations can use blockchain to track and record every transaction, creating an unchangeable audit trail. This allows for real-time monitoring of financial activities and helps detect any fraudulent or suspicious transactions.

Moreover, blockchain technology enables data sharing and collaboration between financial institutions, regulatory bodies, and auditors. With the use of smart contracts, organizations can automate the auditing process and ensure compliance with regulations. Blockchain-based audits provide a higher level of accuracy and transparency, reducing the risk of fraud and enhancing the effectiveness of financial oversight.

Blockchain in Supply Chain Management: Ensuring Authenticity and Transparency

Fraud and data tampering are major concerns in supply chain management. The complex and global nature of supply chains makes them vulnerable to various fraudulent activities, such as counterfeit products, unauthorized changes to product information, and theft. However, blockchain technology offers a solution to these challenges by ensuring the authenticity and transparency of supply chain processes.

1. Product Authentication

Counterfeit products pose a significant threat to supply chains, resulting in financial losses and damage to brand reputation. Blockchain can address this issue by providing an immutable and transparent record of each product’s journey through the supply chain. By using blockchain-based platforms, manufacturers can create digital certificates for products, enabling customers and other stakeholders to verify their authenticity. This not only prevents counterfeit products from entering the market but also ensures that customers receive genuine and high-quality products.

Blockchain also enables the tracking of products from their origin to the point of sale. Each time a product changes hands, the transaction is recorded on the blockchain, creating a permanent and transparent record. This tracking capability not only prevents the unauthorized alteration of product information but also enables end-to-end visibility, allowing organizations to identify and address any issues or bottlenecks in the supply chain.

2. Supply Chain Transparency and Efficiency

Blockchain technology can enhance the transparency and efficiency of supply chain processes by providing real-time access to information for all stakeholders. By recording every transaction on the blockchain, organizations can create a transparent and verifiable history of the movement of goods. This allows stakeholders to trace the origin of raw materials, monitor the progress of products at each stage of the supply chain, and ensure compliance with regulations.

Moreover, blockchain-based platforms enable the automation of supply chain processes through the use of smart contracts. Smart contracts can automatically execute predefined actions when certain conditions are met, reducing the need for manual intervention and ensuring the accuracy and efficiency of supply chain operations. This automation minimizes the risk of fraud and human error, resulting in cost savings and improved productivity.

3. Preventing Fraudulent Activities

Blockchain technology can prevent various fraudulent activities in supply chains, such as double-spending, invoice fraud, and unauthorized changes to product information. By using blockchain-based platforms, organizations can ensure that each transaction is verified and recorded by multiple nodes, making it nearly impossible to alter or manipulate information without the consensus of the network.

Additionally, the use of blockchain enables the creation of a shared and secure database for supply chain participants. This eliminates the need for individual organizations to maintain separate databases, reducing the risk of data breaches and ensuring the integrity of shared information. The transparent and tamper-resistant nature of blockchain instills trust among supply chain participants and helps prevent fraudulent activities.

Blockchain in Healthcare: Protecting Patient Data and Reducing Fraud

The healthcare industry holds vast amounts of sensitive patient data, making it an attractive target for fraudsters. Data breaches, identity theft, and insurance fraud are some of the fraudulent activities that plague the healthcare sector. However, blockchain technology can provide robust solutions to protect patient data, ensure privacy, and reduce fraud.

1. Secure and Immutable Patient Records

Blockchain can facilitate the secure and efficient sharing of patient records among healthcare providers while ensuring the privacy and integrity of the data. By using blockchain-based platforms, healthcare organizations can create a decentralized and secure system for storing and sharing patient records. Each record is encrypted and linked to the previous transaction, forming an immutable and tamper-proof chain of information.

This secure and transparent storage of patient records eliminates the need for paper-based documents and centralized databases, reducing the risk of data breaches and unauthorized access. Patients can have greater control over their own medical records, granting or revoking access to healthcare providers as needed. This not only enhances patient privacy but also reduces the chances of identity theft and insurance fraud.

2. Prescription Drug Traceability

Fraudulent activities in the pharmaceutical industry, such as the manufacture and distribution of counterfeit drugs, pose serious risks to patient safety. Blockchain can help address this issue by enabling the traceability of prescription drugs throughout the supply chain. By recording each transaction related to the production and distribution of drugs on the blockchain, organizations can ensure the authenticity and integrity of the drugs.

Furthermore, blockchain technology can prevent the unauthorized alteration of prescription drug information, such as dosage or expiration dates. Any changes made to the drug information are recorded on the blockchain, creating a transparent and verifiable audit trail. This ensures that patients receive genuine and safe medication, reducing the risk of harm due to counterfeit or improperly handled drugs.

3. Insurance Claims and Fraud Prevention

Insurance fraud is a significant challenge faced by the healthcare industry. Fraudulent claims, identity theft, and billing scams result in financial losses and higher insurance premiums. Blockchain technology can help prevent insurance fraud by ensuring the accuracy and transparency of insurance claims.

By using blockchain-based platforms, healthcare providers and insurance companies can create a shared and secure database to verify claims and track the history of claims payments. The decentralized and transparent nature of blockchain ensures that all stakeholders have access to accurate and up-to-date information, reducing the risk of fraudulent claims. Additionally, blockchain allows for the secure sharing of sensitive patient data between healthcare providers and insurance companies, enabling efficient claims processing while protecting patient privacy.

Conclusion

Blockchain technology plays a crucial role in preventing fraud and data tampering across various industries. Its decentralized and transparent nature ensures the authenticity and integrity of transactions, reducing the risks associated with fraud. In finance, blockchain enhances the security of transactions, verifies identities, and improves auditing processes. In supply chain management, blockchain ensures product authenticity, transparency, and prevents fraudulent activities. In healthcare, blockchain protects patient data, enables secure sharing of medical records, and reduces insurance fraud.

By implementing blockchain solutions and adopting best practices, organizations can strengthen their security measures and protect themselves from fraudulent activities. Whether it’s preventing financial fraud, ensuring the integrity of supply chains, or protecting patient data, blockchain technology offers innovative solutions that can revolutionize the way organizations address fraud and data tampering.

For more insights and practical advice on building secure decentralized applications, refer to the article on “Building a Decentralized App: Best Practices and Development Tools” (Thoughts.tech, 2023). This article provides valuable information on the tools and practices developers can implement to ensure the security and integrity of their blockchain applications.

About us

Thoughts.Tech is dedicated to sharing valuable insights on the latest in technology.

Our mission is to not only provide our perspective but also to serve as a platform for diverse viewpoints from others.

Join us as we explore the ever-evolving world of tech and foster meaningful conversations to broaden our collective understanding.

Categories

Subscribe

© 2023 thoughts.Tech All Rights Reserved.