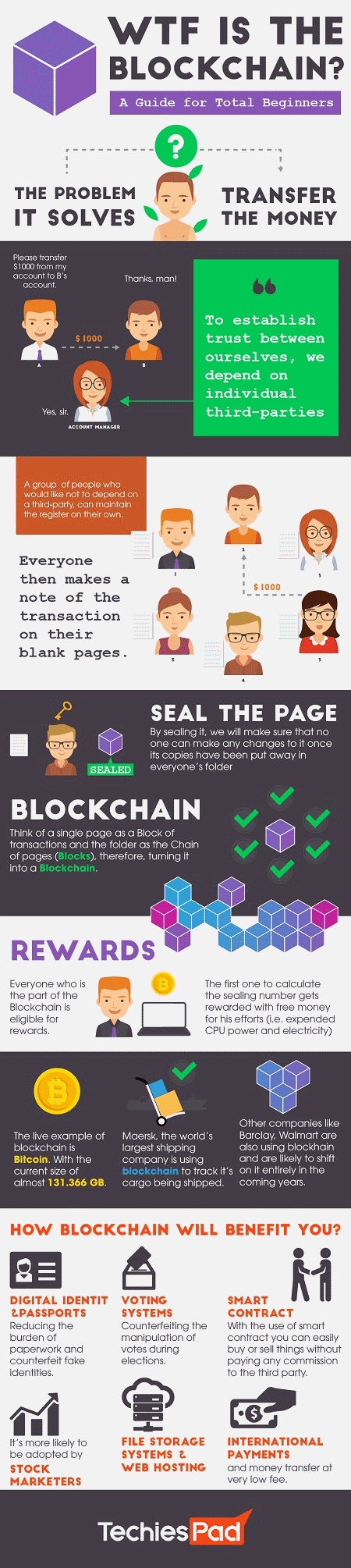

Blockchain technology has revolutionized the way we think about security and trust in the digital age. Its role in preventing fraud and data tampering cannot be overstated. With its decentralized and transparent nature, blockchain provides a powerful solution to combat fraudulent activities and protect sensitive information.

Blockchain operates on a series of interconnected blocks, each containing a unique cryptographic hash. This makes it virtually impossible to alter or tamper with the data stored within. The distributed ledger ensures that all transactions are verified by multiple participants, eliminating the need for a central authority. In fact, according to a recent study, blockchain has the potential to reduce fraud-related costs by up to 80%. By leveraging blockchain technology, organizations can enhance security, increase transparency, and build trust in a digital world plagued by fraud and data tampering.

Introduction

Blockchain technology has gained significant attention in recent years, primarily due to its association with cryptocurrencies like Bitcoin. However, its potential extends far beyond the financial realm. One of the key benefits of blockchain is its ability to prevent fraud and data tampering, making it a valuable tool in various industries.

In this article, we will explore the role of blockchain in preventing fraud and data tampering and how it can be applied in different sectors. We will delve into the technical aspects of blockchain, its benefits, and its potential applications to provide a comprehensive understanding of its role in security and trust.

Before we dive into the details, it’s essential to understand the basics of blockchain technology. If you’re new to the topic, you can start by checking out this article that explains the best practices and development tools for building decentralized applications. It provides valuable insights into the practical implementation of blockchain technology and how it can be utilized beyond cryptocurrencies.

The Fundamentals of Blockchain

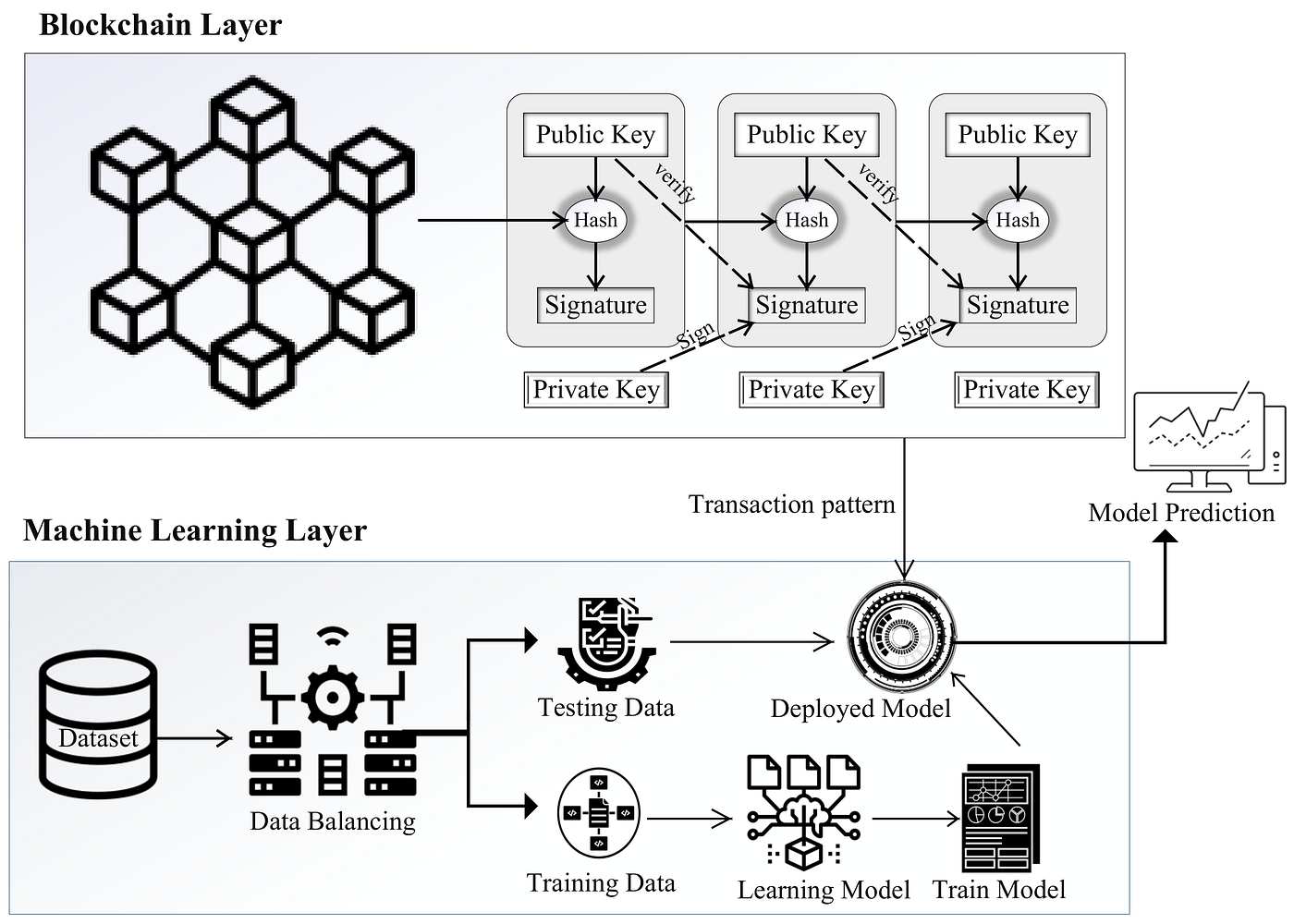

Blockchain is a distributed ledger technology that creates a decentralized and transparent system for recording and verifying transactions. It consists of a chain of blocks, where each block contains a list of transactions. These blocks are linked together using cryptographic hashes, forming an immutable chain.

One of the primary features of blockchain is its decentralized nature. Traditional databases are usually centralized, meaning that they are stored on a single server or controlled by a central authority. In contrast, blockchain operates on a network of computers (nodes), where each node has a copy of the entire blockchain. This decentralized architecture ensures that no single entity has control over the data, making it resistant to fraud and tampering.

In addition to decentralization, blockchain also relies on cryptographic algorithms and consensus mechanisms to verify and validate transactions. These algorithms ensure that the data stored in the blockchain cannot be altered without detection. Furthermore, the consensus mechanisms allow the network participants to agree on the validity of transactions and prevent malicious activities.

The combination of decentralization, cryptography, and consensus mechanisms makes blockchain an ideal solution for preventing fraud and data tampering. Let’s explore some of the specific ways in which blockchain technology can be applied to enhance security and trust in different industries.

1. Supply Chain Management

In supply chain management, maintaining transparency and traceability is crucial to prevent fraud and ensure the authenticity of products. Blockchain technology can play a significant role in achieving these objectives. By recording every transaction and movement of goods on the blockchain, stakeholders can easily verify the origin, location, and condition of products throughout the supply chain.

For example, let’s consider the food industry. With blockchain, each participant in the supply chain, from farmers to distributors to retailers, can record relevant information about the food products, such as the source of ingredients, production methods, and transportation details. This data can be securely stored on the blockchain, making it accessible to all stakeholders while preserving its integrity.

Preventing Counterfeit Products

Counterfeit products are a significant concern in many industries, including pharmaceuticals, luxury goods, and electronics. Blockchain provides an effective solution to this problem by enabling the creation of unique digital identities for each product. These digital identities can contain information such as the manufacturer, date of production, and other relevant details.

Whenever a product is sold or transferred, the transaction is recorded on the blockchain, creating an auditable trail of its journey. Consumers can verify the authenticity of the product by scanning a QR code or using a smartphone app that accesses the blockchain. This ensures that counterfeit products can be easily identified, preventing fraud and protecting consumers.

Ensuring Ethical and Sustainable Practices

Blockchain technology can also be applied to ensure ethical and sustainable practices in the supply chain. By recording information related to certifications, such as fair trade, organic, or sustainable sourcing, on the blockchain, consumers can make informed decisions about the products they purchase.

Furthermore, blockchain can facilitate the verification of responsible sourcing, ensuring that raw materials are not obtained through exploitative or environmentally damaging practices. By providing transparency in the supply chain, blockchain can incentivize companies to adopt sustainable practices and improve overall accountability.

2. Financial Transactions

The financial sector has been one of the early adopters of blockchain technology, primarily driven by the rise of cryptocurrencies. Blockchain provides a secure and transparent platform for conducting financial transactions, reducing reliance on intermediaries and increasing efficiency.

With traditional financial systems, transactions often involve multiple intermediaries, such as banks, clearinghouses, or payment processors. Each of these intermediaries adds a layer of complexity and increases the risk of fraud or data tampering. In contrast, blockchain allows for peer-to-peer transactions, eliminating the need for intermediaries.

Immutable Transaction Records

Every transaction recorded on the blockchain is immutable, meaning that it cannot be modified or tampered with. This characteristic ensures the integrity of financial records and makes it incredibly difficult for hackers to manipulate transaction data.

Moreover, in a blockchain-based financial system, every participant has access to the same set of transaction records, increasing transparency and reducing the risk of fraud. This transparency can also help in complying with regulatory requirements and conducting audits more efficiently.

Smart Contracts for Automated Transactions

Smart contracts are self-executing contracts with the terms of the agreement directly written into code. These contracts are stored and executed on the blockchain, ensuring transparency, security, and automatic enforcement.

Smart contracts can be used to automate financial transactions, such as payments, loan disbursements, or insurance claims. By eliminating the need for manual intervention, smart contracts reduce the risk of fraud or human error and expedite the settlement process.

3. Identity Verification

Identity theft and fraud are significant concerns in the digital age. Traditional methods of identity verification, such as usernames and passwords, are prone to hacking and can be easily manipulated. Blockchain technology offers a more secure and decentralized approach to identity verification.

With blockchain-based identity systems, individuals have control over their personal information. Instead of relying on a central authority to store and manage identity data, blockchain enables users to create digital identities that are secure, private, and tamper-proof.

Self-Sovereign Identity

Self-sovereign identity is a concept that allows individuals to have full control over their digital identities. Blockchain technology enables the creation of self-sovereign identity systems that give users the ability to authenticate and share their personal information securely and selectively.

In a self-sovereign identity system, individuals can choose which entities or organizations can access their personal data. This empowers users to maintain their privacy while still being able to prove their identity when necessary. Additionally, the tamper-proof nature of blockchain ensures that the shared identity information cannot be altered or falsified.

Reduced Identity Fraud

Implementing blockchain technology for identity verification can dramatically reduce identity fraud. By leveraging cryptographic techniques, such as digital signatures and public-key infrastructure, blockchain-based identity systems provide a higher level of security and trust compared to traditional methods.

Moreover, the decentralized nature of blockchain eliminates the need for centralized identity databases that are susceptible to hacking or data breaches. This decentralization ensures that individuals’ personal information remains secure and reduces the risk of large-scale identity theft.

Conclusion

Blockchain technology has the potential to revolutionize various industries by providing secure and tamper-proof solutions for preventing fraud and data tampering. Whether it’s supply chain management, financial transactions, or identity verification, blockchain offers a decentralized and transparent platform that enhances security, trust, and efficiency.

To explore further real-world applications of blockchain beyond cryptocurrencies and understand the best practices and development tools for building decentralized applications, check out this article for more insights.

Key Takeaways – Blockchain and Its Role in Preventing Fraud and Data Tampering

- Blockchain technology provides a secure and transparent way to record and verify transactions.

- It uses a decentralized network of computers to prevent fraud and tampering with data.

- Each transaction is time-stamped and stored in a block, creating an unbreakable chain.

- Blockchain eliminates the need for intermediaries, reducing the risk of manipulation and fraud.

- The immutability of blockchain makes it highly resistant to hacking or data tampering.

Blockchain technology is an important tool in preventing fraud and data tampering. It uses a decentralized system that makes it nearly impossible for anyone to manipulate or alter information.

By creating a network of computers that verify and record transactions, blockchain ensures transparency and security. This makes it an effective solution for various industries, from finance to healthcare, where trust and data integrity are crucial.